Sitting on the deck of his Hawaii Kai home, Walter Chung shares fond memories of his late mother Violet, who passed away three years ago at the ripe age of 98. “She was the typical Chinese matriarch,” he laughs. “Independent, strong-willed, and most of all, stubborn.”

All jokes aside, the 62-year old engineering professional says getting his mother to accept help when her mobility declined was not easy and her fixed income limited their options. “We tried out a few different care homes, but in the end you get what you pay for.” Nursing homes in Hawaii can cost upwards of $130,000 a year and high occupancy rates means admission into a care facility can take a while.

At the time, Walter was also still supporting his two adult children—one of whom was jetting off to college and putting a $40K tuition charge on his tab. “You have to make a lot of hard decisions,” he says. “Do you spend the money to get your mom top-of-the-line care? Or do you spend the money to get your kid a good college education?”

Walter’s struggles are not uncommon. Nearly 47 percent of middle-aged Americans juggle the responsibility of caring for their children and their aging parents—a group of caregivers widely referred to as the sandwich generation. While the physical and emotional strain of caring for multiple generations of family members is tough, the financial burdens are considerably tougher.

The increasing financial pressures of the sandwich generation

Building financial pressure is due in part to a growing number of young adults struggling to establish financial independence. They’re delaying leaving the family nest and relying on their parents to provide some, if not total, financial support. And who can blame them? The price of living in paradise is not cheap. At state minimum wage, a worker would need to put in 116 hours per week to afford a one-bed room apartment in Hawaii. That’s almost three full-time jobs! Realistically, local parents can expect to be paying for their kids long after they reach adulthood.

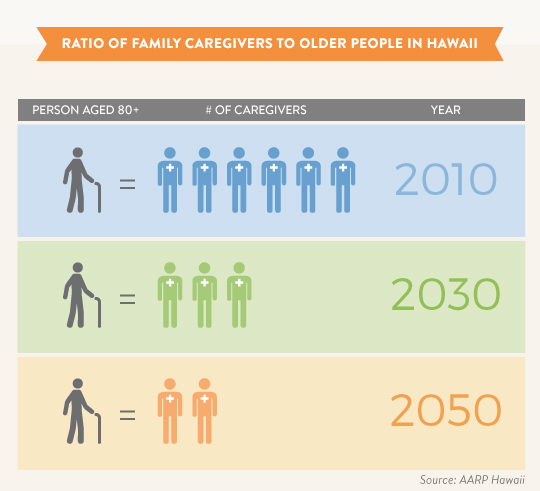

At the same time, the population of seniors is swelling.

The United States Census Bureau estimates that by 2030, 1 in every 5 Americans will be 65-years or older. This dramatic demographic shift—fueled by an aging Baby Boomer population—is expected to create a nationwide elder care crisis. It’s basic supply and demand: too many people needing care, not enough qualified caregivers to provide it. It’s a problem that may be extremely visible here in Hawaii as the state currently boasts the highest life expectancy rate in the country (Source).

How to manage the financial demands of the sandwich generation

State legislators are well aware of the impending caregiver shortage. On July 6, 2017, Hawaii passed a groundbreaking bill that will provide financial relief to the island’s 154,000 unpaid, family caregivers. Senate Bill 534/House Bill 607, also known as the Kupuna Caregivers Act, will help working family caregivers pay for respite care—a benefit of up to $70 a day.

Without siblings to help share the cost of caring for his mother, it’s something Walter—who paid for most of his mother’s care out-of-pocket—would have considered helpful. “With seventy dollars a day, I could have hired someone to take my mom grocery shopping, to the grave to visit dad, or even help sort her weekly medication.”

Hawaii is the first state in the country to invest in a care infrastructure—serving as a national model for other states looking to do the same. The bill is testament to Hawaii’s deep seated cultural expectation of caring for aging family members. “You don’t think about the sacrifices you’re making,” echoes Walter. “You don’t think about the money you’re spending, the missed days at work, the weekends spent at doctor’s appointments. You just do it. It’s family.”

Walter did get some financial relief with his mother’s long term care policy. “It wasn’t enough to get the level of care she needed, but it still helped.”

Long term care insurance is one way to ease hefty long term care costs—an expense most people don’t realize is not covered by Medicare. Since policy premiums typically get more expensive as you age, the earlier you secure long term care insurance, the better.

Some families cope with growing caregiving responsibilities by moving aging parents into their own home. It’s cheaper than a nursing home or assisted living facility. Plus, the cost of any medically necessary home improvements, like adding a wheelchair ramp or handrails, may qualify as a medical tax deduction (see Capital Expenses).

Embracing a multigenerational household also gives children an opportunity to care for their grandparents. It perpetuates cultural values and perhaps sets expectations for them to care for you when the time comes.

When asked if he had one piece of advice to current or future members of the sandwich generation, Walter says, “Start thinking about how you’re going to care for your parents now, before they need it.”

If you are interested in learning more about how home care services can help you manage growing caregiving responsibilities, call Home Care by ALTRES Medical at (808) 591-4930.

Sitting on the deck of his Hawaii Kai home, Walter Chung shares fond memories of his late mother Violet, who passed away three years ago at the ripe age of 98. “She was the typical Chinese matriarch,” he laughs. “Independent, strong-willed, and most of all, stubborn.”

All jokes aside, the 62-year old engineering professional says getting his mother to accept help when her mobility declined was not easy and her fixed income limited their options. “We tried out a few different care homes, but in the end you get what you pay for.” Nursing homes in Hawaii can cost upwards of $130,000 a year and high occupancy rates means admission into a care facility can take a while.

At the time, Walter was also still supporting his two adult children—one of whom was jetting off to college and putting a $40K tuition charge on his tab. “You have to make a lot of hard decisions,” he says. “Do you spend the money to get your mom top-of-the-line care? Or do you spend the money to get your kid a good college education?”

Walter’s struggles are not uncommon. Nearly 47 percent of middle-aged Americans juggle the responsibility of caring for their children and their aging parents—a group of caregivers widely referred to as the sandwich generation. While the physical and emotional strain of caring for multiple generations of family members is tough, the financial burdens are considerably tougher.

The increasing financial pressures of the sandwich generation

Building financial pressure is due in part to a growing number of young adults struggling to establish financial independence. They’re delaying leaving the family nest and relying on their parents to provide some, if not total, financial support. And who can blame them? The price of living in paradise is not cheap. At state minimum wage, a worker would need to put in 116 hours per week to afford a one-bed room apartment in Hawaii. That’s almost three full-time jobs! Realistically, local parents can expect to be paying for their kids long after they reach adulthood.

At the same time, the population of seniors is swelling.

The United States Census Bureau estimates that by 2030, 1 in every 5 Americans will be 65-years or older. This dramatic demographic shift—fueled by an aging Baby Boomer population—is expected to create a nationwide elder care crisis. It’s basic supply and demand: too many people needing care, not enough qualified caregivers to provide it. It’s a problem that may be extremely visible here in Hawaii as the state currently boasts the highest life expectancy rate in the country (Source).

How to manage the financial demands of the sandwich generation

State legislators are well aware of the impending caregiver shortage. On July 6, 2017, Hawaii passed a groundbreaking bill that will provide financial relief to the island’s 154,000 unpaid, family caregivers. Senate Bill 534/House Bill 607, also known as the Kupuna Caregivers Act, will help working family caregivers pay for respite care—a benefit of up to $70 a day.

Without siblings to help share the cost of caring for his mother, it’s something Walter—who paid for most of his mother’s care out-of-pocket—would have considered helpful. “With seventy dollars a day, I could have hired someone to take my mom grocery shopping, to the grave to visit dad, or even help sort her weekly medication.”

Hawaii is the first state in the country to invest in a care infrastructure—serving as a national model for other states looking to do the same. The bill is testament to Hawaii’s deep seated cultural expectation of caring for aging family members. “You don’t think about the sacrifices you’re making,” echoes Walter. “You don’t think about the money you’re spending, the missed days at work, the weekends spent at doctor’s appointments. You just do it. It’s family.”

Walter did get some financial relief with his mother’s long term care policy. “It wasn’t enough to get the level of care she needed, but it still helped.”

Long term care insurance is one way to ease hefty long term care costs—an expense most people don’t realize is not covered by Medicare. Since policy premiums typically get more expensive as you age, the earlier you secure long term care insurance, the better.

Some families cope with growing caregiving responsibilities by moving aging parents into their own home. It’s cheaper than a nursing home or assisted living facility. Plus, the cost of any medically necessary home improvements, like adding a wheelchair ramp or handrails, may qualify as a medical tax deduction (see Capital Expenses).

Embracing a multigenerational household also gives children an opportunity to care for their grandparents. It perpetuates cultural values and perhaps sets expectations for them to care for you when the time comes.

When asked if he had one piece of advice to current or future members of the sandwich generation, Walter says, “Start thinking about how you’re going to care for your parents now, before they need it.”

If you are interested in learning more about how home care services can help you manage growing caregiving responsibilities, call Home Care by ALTRES Medical at (808) 591-4930.